Inventory List For Renters Insurance Claims

Inventory List For Renters Insurance Claims - There are a lot of affordable templates out there, but it can be easy to feel like a lot of the best cost a amount of money, require best special design template. Making the best template format choice is way to your template success. And if at this time you are looking for information and ideas regarding the Inventory List For Renters Insurance Claims then, you are in the perfect place. Get this Inventory List For Renters Insurance Claims for free here. We hope this post Inventory List For Renters Insurance Claims inspired you and help you what you are looking for.

Creating an Inventory List for Renters Insurance Claims

Renters insurance is a crucial safeguard against unexpected events like fire, theft, vandalism, or water damage. However, having a policy is only half the battle. To successfully file a claim and receive fair compensation for your losses, you need a detailed inventory list of your belongings.

Why an Inventory List is Essential

Imagine a fire ravages your apartment. You’re safe, but your belongings are destroyed. Now you have to remember everything you owned, its approximate value, and when you acquired it. Trying to recall these details under stress can be overwhelming and lead to inaccurate claims.

An inventory list serves as a comprehensive record of your possessions, providing documented proof of ownership and value. It makes the claims process significantly smoother and increases your chances of receiving adequate reimbursement to replace your lost or damaged items. Without it, the insurance company may question your claim, leading to delays, reduced payouts, or even denial.

What to Include in Your Inventory List

Your inventory list should be as detailed as possible. A simple list of items isn’t enough; you need specific information for each entry. Here’s a breakdown of the key elements:

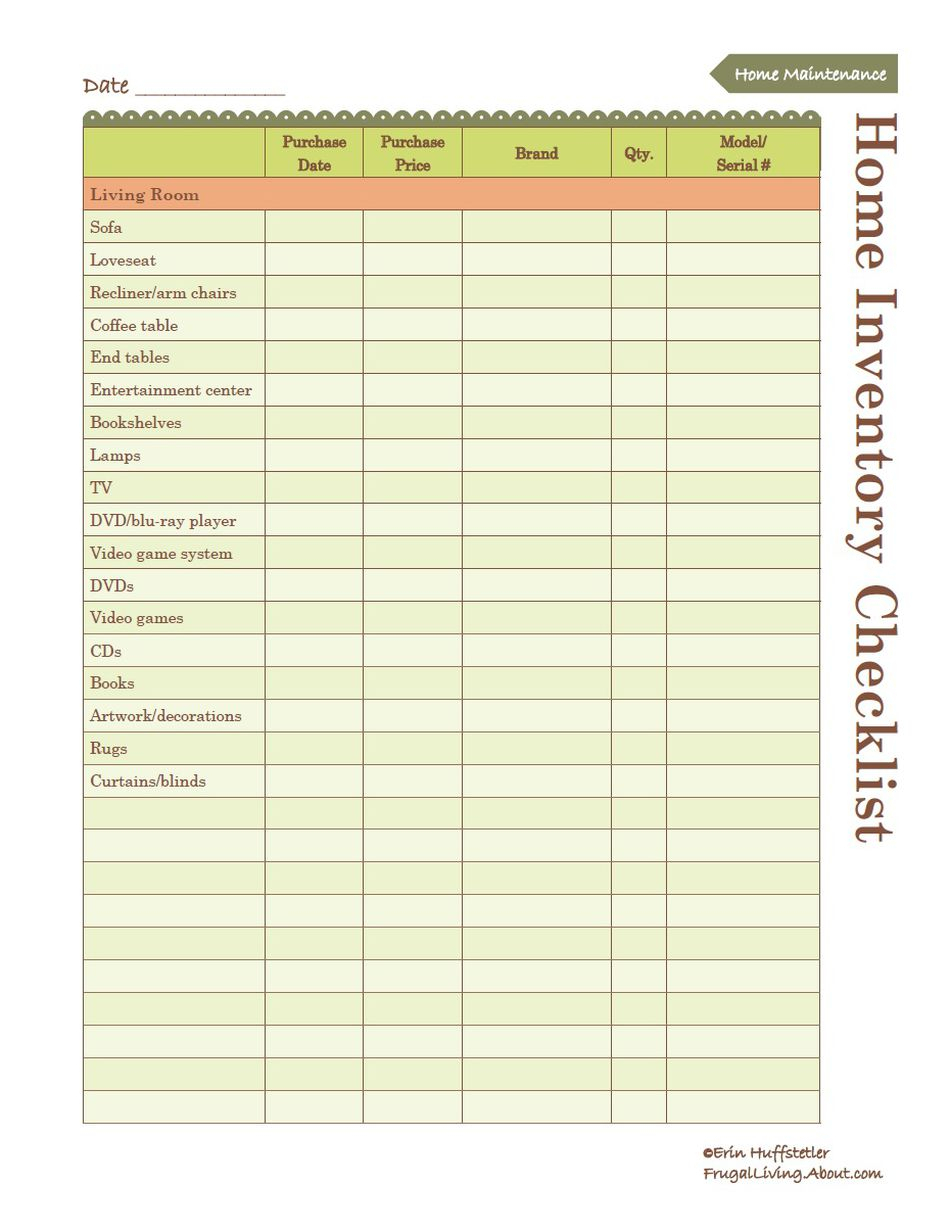

- Item Description: Be specific. Instead of “TV,” write “Samsung 55-inch Smart TV, Model UN55TU7000FXZA.” Instead of “laptop,” write “Apple MacBook Pro 13-inch, 2020 model, 512GB SSD, Space Gray.”

- Quantity: Note the number of each item. For example, “5 bath towels, white, different brands.”

- Date of Purchase: Estimate the date as accurately as possible. If you don’t remember the exact date, approximate the month and year.

- Purchase Price: State the original purchase price. If you can’t remember, research the item online to get an estimated current retail price.

- Place of Purchase: Indicate where you bought the item (e.g., Amazon, Best Buy, Target).

- Current Value: Estimate the current value of the item. This might be less than the original purchase price due to depreciation. Consider if you have a replacement cost or actual cash value policy (more on that later).

- Serial Number (if applicable): Record serial numbers for electronics, appliances, and other valuable items. This helps identify the specific item and can be crucial if it’s stolen.

- Photographs or Videos: Visual documentation is incredibly valuable. Take clear photos or videos of each item. Include shots of serial numbers and any unique identifying marks.

- Receipts and Appraisals: Keep copies of receipts, especially for expensive items. Appraisals are essential for valuable jewelry, art, or collectibles.

Organizing Your Inventory List

A well-organized inventory list is easier to use and more persuasive to your insurance company. Here are a few organizational strategies:

- By Room: Organize your list by room (e.g., living room, bedroom, kitchen). This makes it easier to account for everything and provides a logical structure.

- By Category: Group similar items together (e.g., electronics, clothing, furniture). This can simplify the process of estimating values and comparing prices.

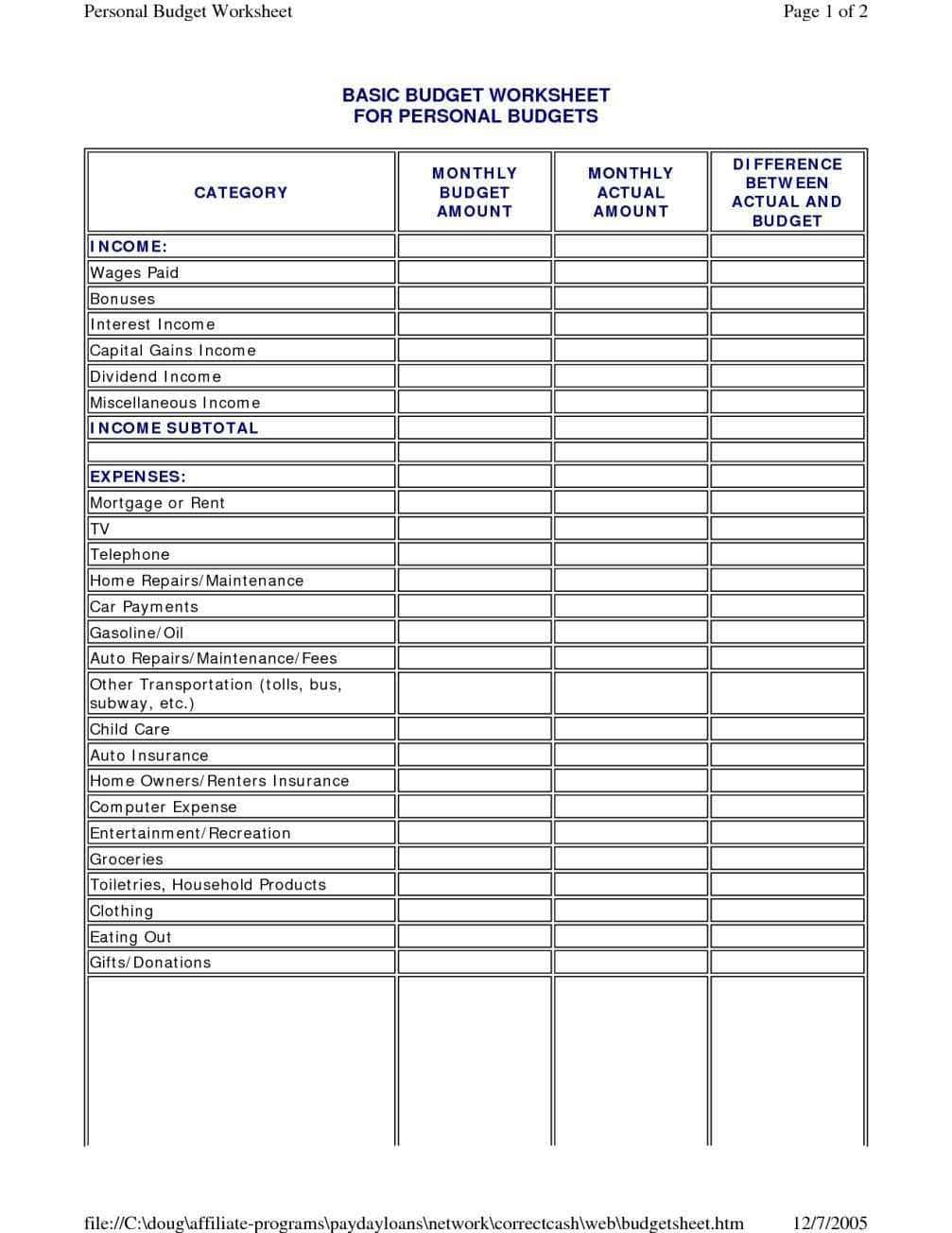

- Spreadsheet Software: Use a spreadsheet program like Microsoft Excel or Google Sheets. This allows you to create columns for each detail (item description, quantity, date of purchase, etc.) and easily sort and filter the data.

- Inventory Apps: Several mobile apps are specifically designed for creating home inventory lists. These apps often include features like barcode scanning, photo storage, and cloud backup. Examples include Sortly, Encircle, and Nest Egg.

Replacement Cost vs. Actual Cash Value

Understanding the difference between replacement cost and actual cash value (ACV) is vital for accurately assessing your loss and filing your claim.

- Replacement Cost: This covers the cost of replacing the item with a brand new one of similar kind and quality, regardless of its age or condition. This is generally the preferred option, as it allows you to fully restore your belongings.

- Actual Cash Value (ACV): This covers the cost of the item minus depreciation. Depreciation reflects the wear and tear and loss of value due to age. You will receive less money with an ACV policy than with a replacement cost policy.

When creating your inventory list, consider which type of coverage you have. For replacement cost, estimate the current retail price of a new item. For ACV, estimate the item’s current value considering its age and condition.

Tips for Maintaining Your Inventory List

An inventory list is not a one-time task. It’s an ongoing process that requires regular updates. Here are some tips for maintaining an accurate and up-to-date list:

- Update Regularly: Review your inventory list at least once a year. Add new purchases, remove items you’ve discarded, and update values as needed.

- Store Securely: Keep your inventory list in a safe and accessible location, such as a cloud storage service or a fireproof safe. Don’t keep it only on your computer.

- Photograph New Purchases: Take photos of new items as soon as you acquire them. Store these photos with your inventory list.

- Review Receipts: Regularly review your receipts and add any missing items to your inventory list.

- Consider a Video Walkthrough: Create a video walkthrough of your apartment, narrating the contents of each room. This provides a visual record of your possessions.

After a Loss: Using Your Inventory List

If you experience a loss covered by your renters insurance, your inventory list will be invaluable. Here’s how to use it:

- Contact Your Insurance Company: Report the loss to your insurance company as soon as possible.

- Provide Your Inventory List: Submit your inventory list to the insurance adjuster. This will provide them with a detailed record of your losses.

- Review Your Policy: Familiarize yourself with your policy’s terms and conditions, including coverage limits, deductibles, and claim filing deadlines.

- Cooperate with the Adjuster: Answer the adjuster’s questions honestly and provide any additional information they request.

- Obtain Estimates: Get estimates for repairing or replacing damaged items.

- Negotiate Your Settlement: If you disagree with the insurance company’s settlement offer, be prepared to negotiate. Your inventory list and supporting documentation will be essential during this process.

Creating and maintaining an inventory list for renters insurance claims might seem tedious, but it’s a worthwhile investment of your time and effort. It can save you considerable stress and financial loss in the event of a covered incident, ensuring you receive the compensation you deserve to rebuild your life.

857×712 renters insurance inventory form form resume examples kwkdpkyjn from www.contrapositionmagazine.com

857×712 renters insurance inventory form form resume examples kwkdpkyjn from www.contrapositionmagazine.com  1185×1534 insurance inventory list template fabtemplatez from www.fabtemplatez.com

1185×1534 insurance inventory list template fabtemplatez from www.fabtemplatez.com  728×546 renters insurance from www.slideshare.net

728×546 renters insurance from www.slideshare.net  1600×1157 renters insurance form table stock image image housing from www.dreamstime.com

1600×1157 renters insurance form table stock image image housing from www.dreamstime.com  600×730 home inventory template excellent expedite insurance from doctemplates.us

600×730 home inventory template excellent expedite insurance from doctemplates.us  298×230 home inventory list insurance forms templates fillable from www.pdffiller.com

298×230 home inventory list insurance forms templates fillable from www.pdffiller.com  950×1231 contents insurance checklist spreadsheet printable home from db-excel.com

950×1231 contents insurance checklist spreadsheet printable home from db-excel.com  1007×1304 contents insurance checklist spreadsheet personal property from db-excel.com

1007×1304 contents insurance checklist spreadsheet personal property from db-excel.com Inventory List For Renters Insurance Claims was posted in June 12, 2025 at 12:59 pm. If you wanna have it as yours, please click the Pictures and you will go to click right mouse then Save Image As and Click Save and download the Inventory List For Renters Insurance Claims Picture.. Don’t forget to share this picture with others via Facebook, Twitter, Pinterest or other social medias! we do hope you'll get inspired by ExcelKayra... Thanks again! If you have any DMCA issues on this post, please contact us!